[ad_1]

It has been greater than a 12 months because the NFT increase in 2021. In keeping with NFTGO, the market cap of NFTs peaked at $36.8 billion in March 2022. Because the market later cooled, the buying and selling quantity and market cap of NFTs began to shrink. This crypto novelty expanded its affect past the crypto group and fostered an enormous market, which additionally gave rise to the mix of NFTs and DeFi. The market has witnessed the looks of NFT lending platforms, NFT aggregators, and NFT derivatives markets, which constitutes the second debut of DeFi Lego enabled by NFTs. Nonetheless, one wonders whether or not these merchandise had been constructed to satisfy actual market calls for and if they’ve created a false proposition that lacks any worth for market participation. In the present day, we’ll dive into whether or not NFT-fi is a possible development and if it can earn market recognition.

It has been greater than a 12 months because the NFT increase in 2021. In keeping with NFTGO, the market cap of NFTs peaked at $36.8 billion in March 2022. Because the market later cooled, the buying and selling quantity and market cap of NFTs began to shrink. This crypto novelty expanded its affect past the crypto group and fostered an enormous market, which additionally gave rise to the mix of NFTs and DeFi. The market has witnessed the looks of NFT lending platforms, NFT aggregators, and NFT derivatives markets, which constitutes the second debut of DeFi Lego enabled by NFTs. Nonetheless, one wonders whether or not these merchandise had been constructed to satisfy actual market calls for and if they’ve created a false proposition that lacks any worth for market participation. In the present day, we’ll dive into whether or not NFT-fi is a possible development and if it can earn market recognition.

Determine 1: Market Cap & Quantity of NFTs | Supply: nftgo.com | As of June 1, 2022

There are lots of NFT liquidity options and NFT structured merchandise in right this moment’s market:

1. NFT fragmentation: FT tokens (similar to ERC20 tokens) which are issued by dividing the possession of helpful NFTs. NFT fragmentation tasks embrace Fractional.artwork, NFTX, and many others.

2. NFT lending markets: Holders can borrow short-term loans by collateralizing their NFTs with out promoting them. Outstanding NFT lending markets embrace BendDAO, NFTfi, and Drops DAO.

3. NFT leasing: Holders earn rents by leasing NFTs to customers in want. NFT leasing tasks embrace Double, reNFT, and many others.

4. NFT aggregators: These aggregators, similar to Gem.xyz, deliver collectively the transaction information of a number of NFT exchanges, receive the perfect NFT transaction value in a single cease, and supply customers with elevated liquidity and extra choices.

5. NFT derivatives: NFT derivatives embrace NFT choices like Putty, in addition to NFT perpetual futures contracts similar to NFTprep.

These tasks are early makes an attempt to deliver collectively NFTs and DeFi. Particularly, NFT fragmentation tasks and NFT aggregators handle the issues of poor NFT liquidity and excessive market threshold. NFT lending markets and NFT leasing tasks additionally give attention to bettering NFT liquidity and capital utilization. In the meantime, NFT derivatives are extra complicated structured merchandise constructed to enhance capital utilization. Nonetheless, these tasks haven’t been in a position to obtain large-scale adoption as a result of they face limitations when it comes to the underlying NFT logic and the event house. Subsequent, we’ll discover the true calls for and false propositions of NFTs.

Actual Calls for

1. The capital utilization of NFTs must be improved, permitting holders to collateralize their NFTs for partial liquidity when operating out of money.

2. The liquidity drawback of NFTs needs to be addressed, enabling holders to rapidly purchase/promote the NFTs they personal.

False Propositions

Did the capital utilization of NFTs go increased?

The issue of NFTs’ capital utilization will be seen in two features: 1) Customers must rapidly purchase and promote NFTs, and the transaction frequency shouldn’t be affected by the poor liquidity of NFTs; 2) Customers ought to be capable to rapidly alternate their NFTs for liquidity and procure money for different functions. With regards to FT tokens, capital utilization will be improved via staking, leverage, and many others. Nonetheless, within the NFT market, there are just a few methods via which customers can enhance their capital utilization. As well as, combining finance with NFT considerably will increase the training value. Proper now, most NFT holders nonetheless depend on the “purchase low and promote excessive” technique. Furthermore, most such holders usually are not the goal person of NFT lending tasks as a result of solely blue-chip NFTs with sound liquidity and worth consensus are accepted.

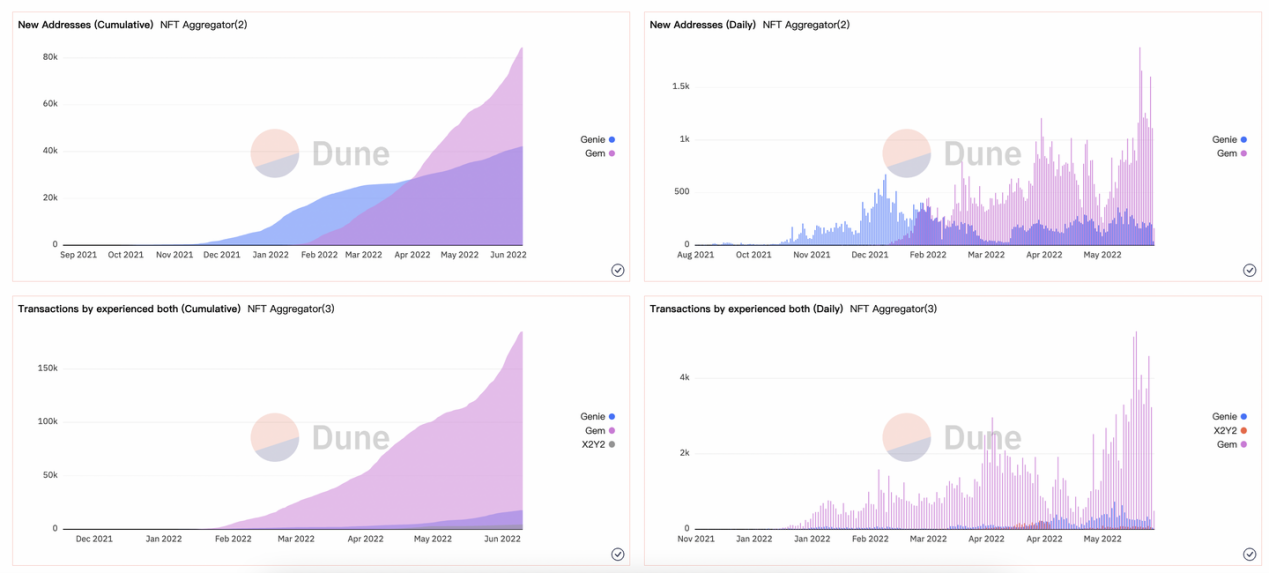

When it comes to the general market scale, most customers are absorbed by secondary markets and aggregators with low working thresholds, and so they haven’t achieved any main enchancment in capital utilization. As proven in Determine 2, the variety of new addresses of Genie and Gem, two NFT aggregators, has been on a gentle rise, with more and more frequent each day transactions. Nonetheless, because the buying and selling quantity and transaction frequency of the 2 have been hit by the sluggish market circumstances of NFTs, Genie and Gem have but to succeed in their most potential for bettering the capital utilization of NFTs.

Determine 2: New Addresses and Transactions of NFT Aggregators | Supply: Dune @sohwak

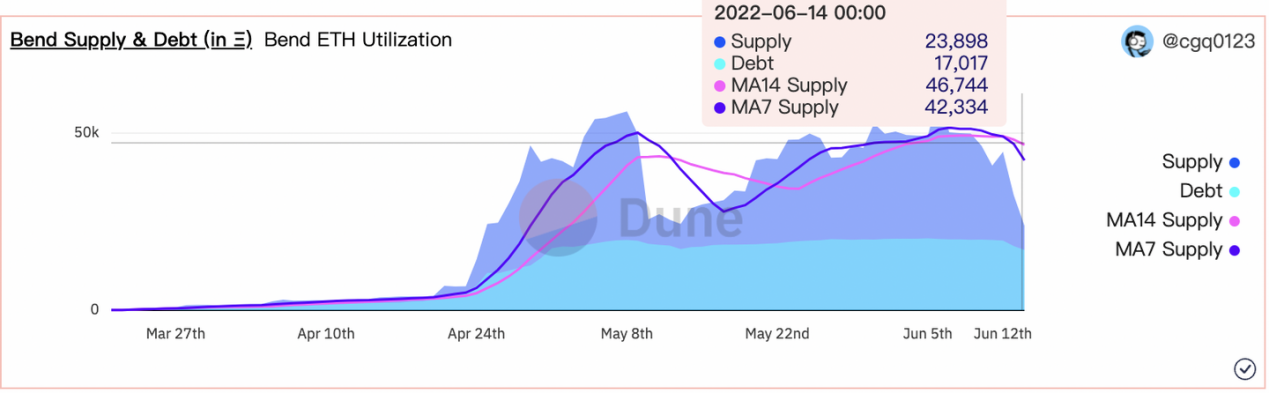

Let’s flip to the capital utilization of mainstream lending tasks. BendDAO is a lending market based mostly on the liquidity pool mannequin the place holders can borrow ETH from the pool after collateralizing their blue-chip NFTs. Because of current market fluctuations, a considerable amount of ETH deposit in BendDAO’s liquidity pool has been withdrawn, which resulted in decreased ETH provide. But, the ETH loans have remained at round 19,000 ETH, whereas the MA14 provide stands at 46,000. As such, we will make the tough estimate that BendDAO’s capital utilization is about 41%.

Determine 3: Bend ETH Utilization | Supply: [email protected]

Observe: MA14 refers back to the transferring common in 14 days, whereas MA7 signifies the transferring common in 7 days

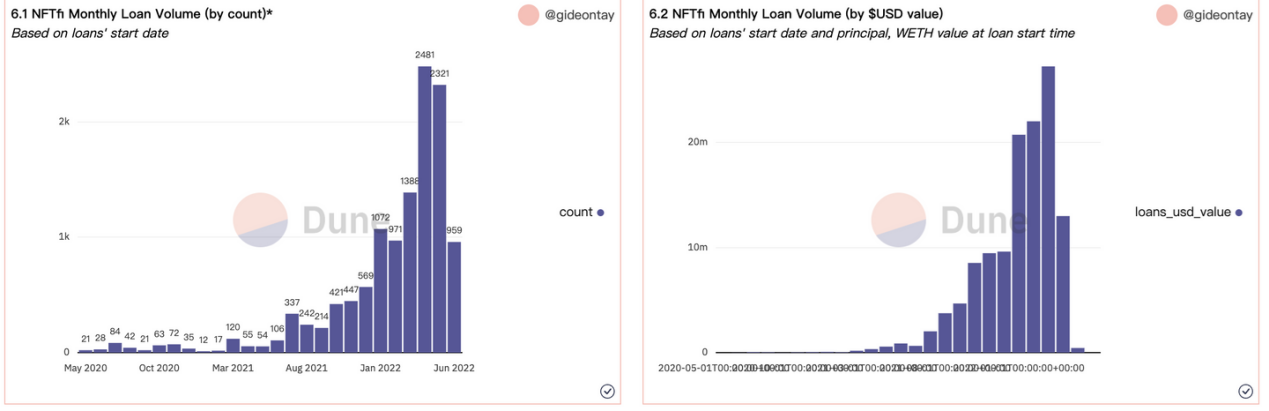

NFTfi is a lending market following the P2P mannequin. The quantity, rate of interest, and period of loans on NFTfi are collectively decided by liquidity suppliers and NFT lenders, which is extra versatile when it comes to the mortgage fee. The variety of month-to-month loans provided through NFTfi elevated from 21 in Could 2020 to 2,000+ in Could 2022, and the utmost month-to-month mortgage quantity reached $27.52 million (March 2022), however this determine solely accounted for 1% of the market cap of blue-chip NFTs (as reported by NSN-BlueCHIP 10).

Determine 4: NFTfi Month-to-month Mortgage Quantity by Rely/Worth | Supply: [email protected]

JPEG’d can also be a P2P mannequin lending protocol, and it now solely gives collateralized lending for Cryptopunks, EtherRocks, BAYC, and MAYC. After staking NFT, holders will obtain PUSD, a stablecoin, offered by the protocol from the pool. Moreover, JPEG’d additionally contains a 32% capital utilization restrict on lending.

In fact, there are additionally different early-stage NFT derivatives platforms, however they haven’t launched any mature merchandise, so we couldn’t analyze their capital utilization. Regardless of that, it’s foreseeable that such NFT derivatives will include increased studying prices as they’re merchandise designed for skilled merchants with higher danger urge for food. As such, their progress potential is proscribed in right this moment’s NFT market.

Asset Pricing and Liquidation Dangers?

The pricing of NFTs has been so incessantly mentioned that it has now turn into a cliché. Persons are involved with the difficulty as a result of the value swings of NFTs will expose NFT lending or derivatives to liquidation dangers. Because the NFT costs fell over the current interval, BendDAO has began a number of liquidation auctions.

Though a lot of the lending protocols on the market have adopted over-collateralization, within the face of untamed value swings, many NFTs can be liquidated and bought in marketplaces. This, coupled with the poor liquidity of NFTs, may result in panic promoting, which might create downward value spirals, in the end turning the loans into unhealthy money owed.

The pricing of NFTs is topic to a number of elements. Plus, additionally it is simply manipulated. For instance, large holders might maliciously elevate the ground value after which liquidate the NFTs on goal, and an NFT might take a value plunge because of hacking or good contract loopholes. Furthermore, NFT pricing may be affected by many intangible elements. As an illustration, the value of an NFT might soar if a well-known particular person immediately buys it in giant quantities or if it releases a brand new airdrop plan.

As most lenders can’t precisely estimate the intrinsic worth of their NFTs, they’re susceptible to liquidation in the event that they borrowed loans or utilized leverage. That is additionally one of many the explanation why NFT lending and derivatives haven’t gained mass adoption: Blue-chip NFT holders are apprehensive that they may endure losses within the above eventualities, which is why they’re reluctant to collateralize their NFTs.

Do blue-chip NFT holders actually need NFT loans?

All NFT lending markets give attention to blue-chip NFTs, however most blue-chip NFT holders usually are not in nice want of loans. To start with, such holders care extra about their possession of the NFTs, similar to billionaires wouldn’t use their collectibles as collateral for loans. Secondly, NFT loans include unknown dangers, and lots of blue-chip NFT holders refuse to use for such loans after weighing the dangers in opposition to the advantages. Thirdly, making use of for NFT loans comes with excessive studying prices, and never each person can perceive the precept behind such loans.

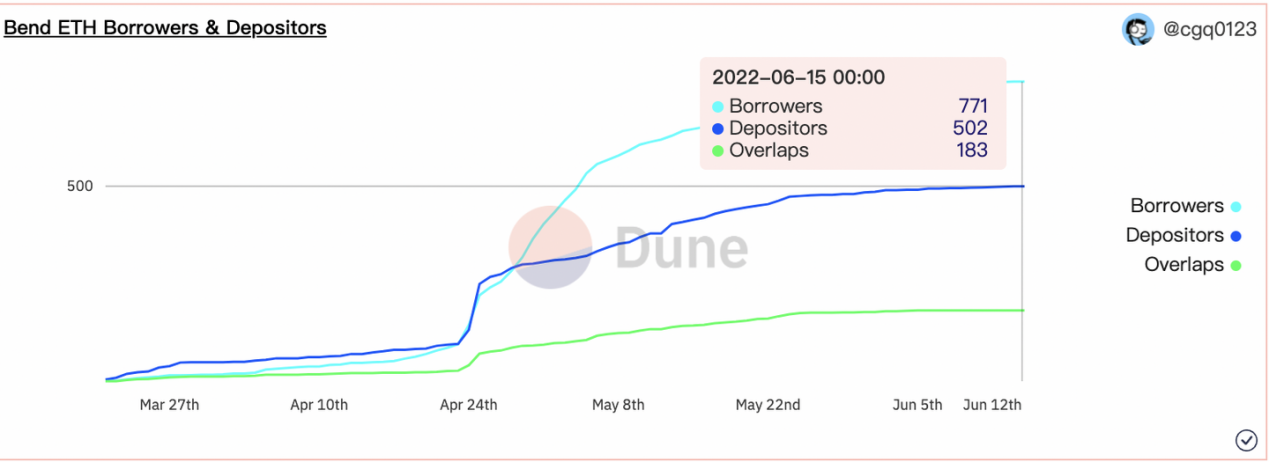

Let’s examine the person base of the key NFT lending tasks. As of June 15, there are about 2.4 million holders within the NFT market, of which 27,833 maintain blue-chip NFTs (a person will probably be thought to be a blue-chip NFT holder so long as he owns a minimum of one such NFT), based on NFTGO. There are 771 debtors on BendDAO, 1,038 on NFTfi, and 51 on Arcade. As customers should first deposit/collateralize their NFTs earlier than making use of for a mortgage, we will regard all these debtors as blue-chip NFT holders. It’s due to this fact clear that almost all blue-chip NFT holders usually are not customers of NFT lending markets.

Determine 5: Bend ETH Debtors & Depositors | Supply: [email protected]

Might NFT-fi tasks retain customers with the identical outdated incentive?

Lending or derivatives tasks additionally bear the duty of bettering the protocol’s liquidity. Most such tasks provide native tokens as the inducement for recruiting NFT holders and depositors as they go stay. On this regard, these tasks resemble DeFi liquidity mining platforms that entice speculators with excessive APYs. Nonetheless, the issue is that they’d not be capable to preserve such liquidity if the APYs went down. Attracting customers with token incentives remains to be the identical outdated strategy. Although this technique might create a big person base on the very starting, nobody is aware of whether or not the protocol might retain customers.

For instance, when the venture was first launched, BendDAO airdropped BEND tokens to customers who had deposited blue-chip NFTs and ETH. It additionally makes use of BEND as a subsidy when paying pursuits. Nonetheless, the rate of interest went down when the BEND value dropped, which slowed down the expansion fee of recent customers.

As such, attracting customers with excessive APYs is simply step one. To retain new customers, they have to additional discover the lending mechanisms, handle the oracle pricing subject, and mitigate the liquidation dangers. Initiatives ought to develop extra versatile merchandise whereas increasing the scope of NFT lending. Final however not least, they may additionally present danger critiques, decrease the training value, and provide extra satisfying person experiences.

Conclusion

The evolution from NFT to NFT-fi is a course of wherein a market grows from its infancy to a extra mature stage. Nonetheless, additionally it is inevitably a course of that’s stuffed with doubts, traps, and issues. As NFT-fi tasks search to satisfy actual calls for, they will even need to face doubts that they’re stating false propositions. In the present day’s NFT market is sort of a new child baby who must develop up and stick via challenges. Though NFT-fi may be a fantastic try, there may be nonetheless an extended technique to go, and NFT-fi tasks need to preserve exploring their underlying logic to earn market recognition.

[ad_2]

Source link

![Guide to Using Multisig Wallets to Secure Your Crypto [2023]](https://bitscoop.io/wp-content/uploads/https://bitpay.com/blog/content/images/2023/03/multisig-wallets-security-bitpay.jpg)